Imagine, if you will, that you slipped on the ice and landed pretty hard. You were lucky enough not to break anything, but you definitely threw your back out, and it hurts like a son-of-a-gun. Thankfully, you have health insurance through Obamacare. With your card in hand, you limp off to your chiropractor.

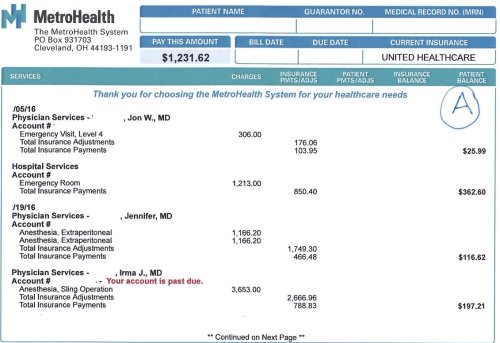

A few weeks later, you get a bill to the tune of $600. What in the ever-loving…you have health insurance! What is this baloney?

“This” is health insurance, Obama-style. I’m just gonna come out and say it, because it’s my blog and it’s what I do. Face it. Obama and his “affordable” health care is a big, fat, lie.

I work in medical billing. If a policy exists, I’ve pretty much seen it. All major companies Aetna, Blue Cross Blue Shield. GIC Unicare. Neighborhood Health. Medicare. Medicaid. Tufts. United Healthcare. Cigna. Health New England. And so on.

So WHY are you getting a huge bill when you have insurance? Because you’re paying into the system, to cover all the people who don’t have insurance, or waited to purchase on the exchanges until they got sick, or are on some form of Medicaid (state-sponsored plans), and yes, everyone is out to make a buck. So you’re getting a bill because you have a $50 copay per visit. You also have a $6000 deductible. And 20% co-insurance. Oh, and you’re limited to 12 (that’s the usual) visits. Your out-of-pocket expenses cap at $8000.

What does this mean? It means that first and foremost, you have to pay that $6000 deductible before your insurance carrier will even consider footing the bill. You’re responsible for that amount. Until you hit that, your copay won’t go toward your bill, it goes toward that. Boom. You’re $6000 in the hole, and it’s only January 8. Happy New Year! Love, Barack. So you decide to sell your car or beg a rich relative to cover that deductible. Great! Now, when you show up to your appointments, they demand $50 every time you walk through the door. That’s your copay, your share of the bill. (Isn’t it great when everyone pays “their fair share”?) Fine, it’s 50 bucks. You’ll just give up on eating out for a while. You’re limited by your insurance to 12 visits, so that’s another $600 out of your pocket, on top of your $6000 deductible. What does your insurance company pay out per visit? Many of them top out around $40. You have a $50 copay.

Insurance isn’t going to cover jack.

Meanwhile, you’re also still paying a monthly premium. Newsflash: That doesn’t go toward your deductible. It doesn’t go toward your out-of-pocket, either.

You basically just paid the insurance company in order to go to the doctor.

Imagine, again, that you are a 27 year-old male. You’re single, with no serious relationship on the horizon. You have a $400 a month premium for your self-insured (not employer sponsored) BCBS plan. Do you realize you’re paying for pediatric, obstetrical, gynecological, and abortion services?

Why, on God’s green earth, does a healthy, single male need pediatric and OBGYN coverage?

Obamacare, that’s why.

You were forced to have this.

You’re welcome.

(A word of advice. If you are unlucky enough to have a plan like this and you need services, talk to your provider about becoming a cash patient. It may save you a few bucks.)